Bitcoin has a 15-year track record, institutional backing, and a hard supply cap that makes its value proposition legible even to a skeptic. Ethereum has a developer ecosystem, established DeFi infrastructure, and years of battle-tested smart contract execution. Evaluating everything else – the 17,000-plus altcoins currently in circulation – requires a different framework entirely. Most of them will not survive. A handful will. The question is which criteria actually distinguish one from the other before the market delivers its verdict.

What “Altcoin” Actually Covers

The term altcoin means any cryptocurrency other than Bitcoin. It derives from the idea that BTC is the original and everything else is an alternative. The category is enormous and internally inconsistent: it includes Ethereum, Solana, and Cardano in the same bucket as thousands of tokens that have never found a single use case or sustained any meaningful price above their launch level.

The first altcoin was Namecoin, launched in 2011 – three years after Bitcoin – as a fork of the original protocol designed to create a decentralised domain name system. That origin story is instructive. Most altcoins emerge from forks, where a group of developers disagrees with an existing protocol’s direction and breaks off to build something new. The fork inherits the original codebase but pursues different design goals: Bitcoin Cash forked from Bitcoin to increase block size and prioritise transaction throughput; others fork simply to capture speculative interest with minimal differentiation.

Understanding what category an altcoin falls into – payment token, smart contract platform, DeFi protocol, governance token, infrastructure layer – is the starting point for any evaluation. A token with no identifiable category is almost certainly not worth evaluating further.

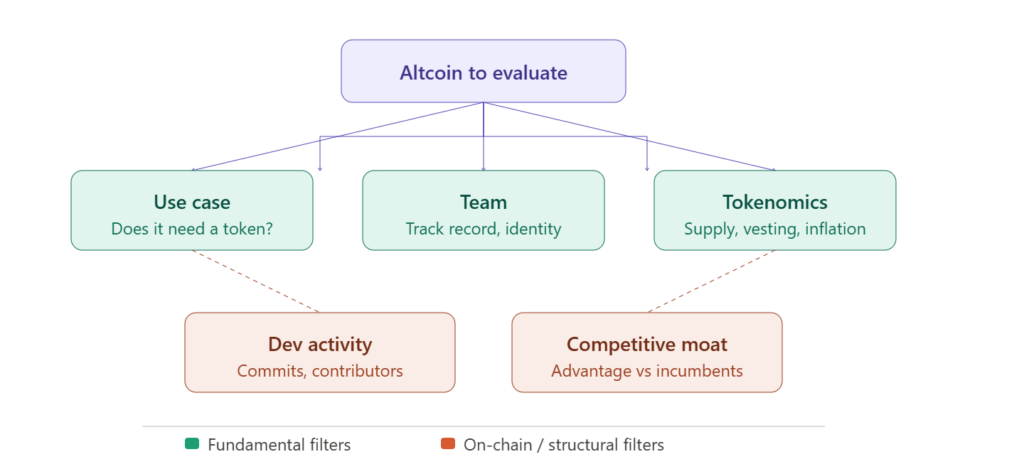

The Five Questions That Actually Matter

Most altcoin analysis gets derailed by price action. An asset that has risen 400% in three months attracts attention regardless of whether there is any underlying justification for the move. Systematic evaluation requires separating price history from fundamentals and asking five specific questions.

First: what problem does this solve, and does the solution require a token? Many altcoins exist because issuing a token is an effective way to raise capital, not because the underlying application requires on-chain scarcity. If the same product could function identically without the token, the token’s long-term value proposition is structurally weak.

Second: who built it and what is their track record? Anonymous founding teams are not automatically disqualifying – Bitcoin’s creator is pseudonymous – but they shift the burden of proof. Verifiable teams with prior experience in cryptography, distributed systems, or relevant industry domains provide a base level of accountability that anonymous projects cannot.

Third: what does the tokenomics look like? Supply schedules, vesting periods for team allocations, and inflation rates matter enormously. A token with 60% of supply held by founders on a 12-month vesting schedule creates predictable selling pressure at unlock dates. Omicron’s rise of 1,000% followed by an equivalent collapse – a pattern repeated across dozens of tokens – is almost always preceded by concentrated supply in few hands.

Fourth: how active is the developer community? On-chain data and public repository activity (commits, contributors, open issues) provide a signal that is harder to manufacture than social media engagement. A protocol with consistent development activity over 18+ months is meaningfully different from one that launched with a white paper and has had minimal subsequent technical work.

Fifth: what is the competitive moat? Altcoins operating in established categories – layer-1 smart contract platforms, DEX protocols, lending markets – compete against incumbents with network effects, liquidity, and developer mindshare. A new entrant needs a specific, articulable advantage to displace existing solutions.

Consensus Mechanisms as a Signal

How an altcoin secures its network is not just a technical detail – it is a window into the design priorities of the team and the token’s economic structure.

Proof of Work altcoins, inherited from Bitcoin’s model, require computational energy to validate transactions. This creates real-world cost that functions as a barrier to attack, but it also means the token must generate sufficient mining revenue to sustain security. For small-cap PoW altcoins, hash rate is usually tiny, making 51% attacks economically feasible with modest resources.

Proof of Stake, used by Ethereum post-merge, Cardano, Solana, and many others, requires validators to lock tokens as collateral. This aligns validator incentives with network health and removes the energy cost of PoW. The tradeoff is that stake concentration can create centralisation risks – if a small number of validators control a majority of staked supply, the network’s censorship resistance is limited.

|

Consensus type |

Examples |

Security model |

Key risk |

|

Proof of Work |

Litecoin, Dogecoin |

Energy cost as an attack barrier |

Low hash rate = vulnerable to 51% attacks |

|

Proof of Stake |

Cardano, Solana, Avalanche |

Staked collateral at risk |

Stake concentration, slashing risks |

|

Delegated PoS |

EOS, TRON |

Elected validators |

Cartel formation among delegates |

|

Proof of Burn |

Slimcoin |

Tokens destroyed to earn rights |

Deflationary but limited adoption |

The consensus mechanism also determines staking economics, which feeds directly into tokenomics. An altcoin with high staking yields paid from token inflation is effectively diluting non-staking holders to reward validators – a dynamic that compounds into significant value destruction for passive holders over multi-year periods.

On-Chain Metrics Worth Tracking

Price is the last signal, not the first. The metrics that precede sustainable price appreciation in altcoin in crypto markets are on-chain: active addresses, transaction volume, total value locked for DeFi protocols, fee revenue, and developer activity.

Active address growth that precedes price appreciation suggests organic adoption. Price appreciation without address growth suggests speculative positioning without underlying utility – a pattern associated with rapid reversals. Total value locked in DeFi protocols measures actual capital deployed in the application, which is a harder metric to fake than social engagement or trading volume on low-liquidity exchanges.

Fee revenue is the closest altcoin equivalent to earnings. A protocol generating meaningful fee revenue from real user activity has a defensible value case. One generating no fees despite high token price is pricing in future adoption that may never materialise.

How to Size Positions When You Find Something Worth Trading

Evaluating an altcoin and trading it are two different decisions. A strong evaluation does not automatically justify a large position, because even genuinely promising altcoins carry execution risk: protocol exploits, regulatory actions, and team failures can eliminate value regardless of the quality of the underlying analysis.

Position sizing in altcoins should account for the higher volatility relative to Bitcoin and Ethereum, the lower liquidity of smaller-cap tokens, and the binary risk of projects that can go to zero. A framework used by experienced traders is to limit individual altcoin exposure to a percentage of portfolio that they could lose entirely without material impact on their overall trading capital – treating each position as a high-conviction wager rather than a portfolio allocation.

Conclusion

Most altcoins fail. That is not a reason to avoid the category – it is a reason to develop specific criteria for identifying the minority that do not. Problem clarity, team accountability, tokenomics structure, developer activity, and competitive position are the five filters that cut through the noise of 17,000 tokens. Apply them before looking at the price chart, not after.